Evangelism

A Letter To MPs To Review Or Overturn The Competition Commission’s Findings

I have written today to my local MP and to ten other MPs whose constituencies contain or border the cinemas under threat from the Competition Commission. However, MPs in the UK are only supposed to act on behalf of their own constituents, so those other 10 MPs may not be able to do anything directly to follow up on my letter.

So I am making publicly available the letter that I’ve written. If you intend to contact your MP you have my permission to attach a copy of this letter to your contact.

The letter in full – you may wish to exclude those paragraphs in square brackets:

Dear Member Of Parliament,

[I am writing to you as both a constituent in one of your areas (East Cambridgeshire), but also on behalf of over 13,700 people that recently signed a petition to protest the sale of cinemas that your constituents currently attend, and those 13,700 people include constituents in each of your areas. I will try to summarise the situation as briefly as possible.]

Cineworld Group plc, which runs one of the largest chains of multiplex cinemas in the UK, late last year purchased City Screen Ltd, which among other activities also runs a chain of independent cinemas. After a referral from the Office Of Fair Trading, the Competition Commission published an initial report in August which they confirmed yesterday, instructing Cineworld Group to sell either the Cineworld or Picturehouse in each area. Cineworld Group intend to sell the Picturehouse in Aberdeen and Bury St. Edmunds and are yet to decide which of the Cambridge cinemas to sell.

I believe this decision is wrong for a number of reasons, and that that the research commissioned into the problem is fundamentally flawed.

- There is no evidence, either supplied by the Commission or independently, that competition is effective in setting prices in this industry. Cinema chains set prices at similar levels in geographic areas, with competition seeming to have a much weaker effect than the local cost of living and other factors, and forcing the sale of one cinema will just bring in another cinema with no obligation to charge lower prices, and when considering the other operators in the market a likelihood that prices will increase.

- Typically, a geographic area the size of Aberdeen is capable of sustaining two cinemas, and of Cambridge and Bury St. Edmunds only one, based on the national average. Counting Cineworld’s cinemas as one, there would still be two operators in Aberdeen and Cambridge, and one in Bury St. Edmunds. While competition has lessened, it has only lessened to the national average, when it was above this originally.

- Following the referral, the OFT published a report in June, where they considered that Cineworld and Picturehouse were operating in different markets. Cineworld is a multiplex, whereas Picturehouses follow an independent or arthouse model. The Competition Commission instead found that these cinemas were in direct competition, yet their deputy chairman Alisdair Smith has admitted since the report was published in an interview on BBC Radio Cambridgeshire that they would expect different buyers for the Cineworld or Picturehouse should they be sold, clearly supporting that the markets are different.

- The research was based on a single adult ticket price, and the likelihood of customers to switch cinemas if prices were to increase by 5%. The Commission’s own research showed that 58% of Picturehouse customers are members and receive discounts on every ticket of more than 5%. Additionally, market statistics show that around 1 in 8 tickets purchased from Cineworld cinemas nationally are under some form of membership discount. The myCineworld scheme offers a greater discount – 10% – to anyone booking online with no commitment, and again the research did not consider this. Cineworld is the only multiplex operator to run such schemes.

The Commission claim to have considered customer feedback in compiling their final report, but have not addressed any of these concerns, which were addressed to them directly prior to the publication of the final report.

The two chains in question currently have the best record in the industry of offering discounts to their customers nationally, and in a like for like comparison in any areas where they operate they are offering lower prices than their competitors. Any enforced sale will not just impact prices for consumers.

- The Picturehouse cinemas offer cafe bars where hot meals and alcohol can be purchased and taken into the screens. The findings from the Commission ignored the role these play in attracting customers, who are looking for a different experience to a normal multiplex cinema.

- The cinemas offer a much wider choice of films, typically at least double the number of films per screen per week than a multiplex, and while a proportion of the revenue comes from films shown at both cinemas, the Picturehouses show a wide range of films and live events not regularly offered at the multiplex cinemas.

- The Picturehouses also offer a range of screenings for parents with young children, senior citizens and those on the autism spectrum and their carers. Very few other cinema chains offer these services and none with the frequency of the Picturehouses.

- These cinemas also support a wider cinema culture in the form of trusts and festivals that take place year round, and are also capable of a wider range of projection – the Cambridge Arts Picturehouse being one of the few cinemas in the country that can still show 70mm films, and they are reliant on existing expertise. Without a Picturehouse, Cambridge and Bury residents would have to travel to London to see these films and Aberdeen residents to Edinburgh, none of which are practical options for most.

Any enforced sale of these cinemas will result in higher prices for your constituents, a loss of the ancillary services and a significant reduction in choice. A comparison to any of the current operators in either market shows that each charges the same or higher for tickets with less discounts, offers less choice in their programming and doesn’t support the ancillary services to the same extent. The sale of these to an independent operator without the resources of a chain behind it could see the cinemas quickly fold; the Bury St Edmunds cinema was in trouble prior to the Picturehouse takeover, and Aberdeen’s Picturehouse is being subsidised by the local council after also running into difficulties, and without the resources of an operator such as City Screen they may soon be back in a similar position.

Before the Commission published its final report, the local council in each area proposed to put in place behavioural remedies, where they would put some measure of price controls on the existing cinemas. Two of the councils gave detailed proposals and had run similar controls previously. The Commission dismissed these proposals on the grounds that they would not increase competition – when the sole purpose of increasing competition is to attempt to restrict prices – and that the OFT would have incurred costs in supporting such schemes. Instead, these costs will be passed directly to your constituents in the form of higher ticket prices.

I would urge you to take the appropriate steps to set aside or overturn the findings of the Commission, on the basis that:

- All of the research showed a clear differentiation in the market between arthouse / independent and multiplex cinemas, which if considered would have negated the findings.

- The findings were based on a flawed assumption of a single ticket price and incorrectly excluded membership schemes. The surveys on which they based their findings excluded these and are therefore fatally flawed.

- There is still a level of competition at least at the national average in these areas following the takeover, so there is no requirement to increase competition further in these areas.

Failing that, I would ask that the behavioural remedies proposed by the local councils be re-examined as these appear to be a better option for your constituents than the structural remedies proposed of selling cinemas.

[I enclosed links to my more detailed research and to other material on the situation, and I would be happy to provide further clarification on anything here:

https://movieevangelist.wordpress.com/competition-commission/

I will be advising those who signed the petition to contact you for your support, and I would expect you all to hear from them in due course, if you haven’t already.

Yours sincerely,

Mark Liversidge]

Cambridgeshire MPs:

Cambridge – Julian Huppert: julianhuppertmp@gmail.com

Huntingdon – Jonathan Djangoly: djanoglyj@parliament.uk

North East Cambridgeshire – Stephen Barclay: stephen.barclay.mp@parliament.uk

North West Cambridgeshire – Shailesh Vara: varas@parliament.uk

South Cambridgeshire – Andrew Lansley: lansleya@parliament.uk

South East Cambridgeshire – James Paice: paicejet@parliament.uk

Suffolk MPs:

West Suffolk – Matthew Hancock: paicejet@parliament.uk

Bury St. Edmunds – David Ruffley: antonia.merrick@parliament.uk

Aberdeen MPs:

Anne Begg: begga@parliament.uk

Malcolm Bruce: milsomr@parliament.uk

Frank Doran: doranf@parliament.uk

The Cineworld / Picturehouse Merger: The Final Decision And Next Steps

After an agonising wait over the last few weeks, the Competition Commission have this morning publised their final report, and have given the news that rational supporters of cinema both feared and, if we’re being honest, expected: that Cineworld group must sell one of their cinemas in each of the three affected areas: Cambridge, Bury St. Edmunds and Aberdeen. Cineworld have in turn published a statement, which would seem to suggest that they will not be appealing the decision (no statement is made that they will appeal) and that they currently plan to sell The Belmont in Aberdeen, rather than either of the Cineworlds there, and also to sell the Abbeygate Picturehouse in Bury St. Edmumds. They have not yet made a decision as to which cinema will be sold in Cambridge.

They have also made specific reference to the cafe in Bury St. Edmunds in their findings, in that it does not need to be retained by any cinema supplier. Given that any purchaser will be required to be in competition with Cineworld by the terms of the findings, the possibilty of that cafe being replaced by another screen or a bland concessions area in an attempt to make the cinema more competitive must surely now be very real.

The Commission also had the offer of putting price controls in place on the Picturehouse cinemas, and all three local councils had shown both a willingness to do this and two had comfirmed they have operated similar schemes in the past. The Commission rejected this, effectively on the grounds that restricting prices wouldn’t encourage competition – when the purpose of competition is solely to restrict prices – and that the Office Of Fair Trading would incur costs. Instead, those costs are likely to be passed directly to consumers.

The Commission are also required to consider any benefits of the merger. What they are not required to do in law is to consider any benefits of the two chains that existed before the merger and have been retained by it, but that would be lost by selling one of the cinemas. Consequently, the findings have overlooked the current state of operation of these cinemas, focused on a single point in law which misrepresents how the industry operates as a whole, and have pursused this point to the detriment of cinema lovers in each of these areas.

This is terrible news for all three areas. I remain of the belief that Cineworld and Picturehouses offer better deals to their customers than any of the other operators, in three key areas: price, programming choice and other services, and I say that as someone who has been to cinemas of every major operator in the past three years. The Competition Commission have ploughed a single-minded furrrow through an industry they do not understand, and have come to the conclusion that allows them to have taken the path of least resistance rather than protecting the desires and needs of customers.

As part of their final report they have published a set of letters from customers, including myself, and even one from the MP for Aberdeen that was send directly to them. I can find no response from them on a single question that was posed to them. Spectactularly, there is a post on their website which actually goes to the extent of summarising the concerns of the 600 people who wrote to them directly, and the 13,700 people who signed the petition to date, and then doesn’t respond to any of it.

If you navigate to my letter, you’ll find that I asked four questions of them the day after the initial report was published. I also wrote to them before the deadline and posed some futher questions, which remain unanswered:

1. Was there no requirement to set a suitable threshold for competition in a given area? The areas concerned seem to have a luxury of competition compared to geographical areas of similar size and population density, and this decision is simply regressing them to the same level as their competitors.When I reviewed the findings initially, I discovered that geographical areas of similar size to Cambridge don’t normally have competition in cinemas, they can normally only sustain one. Consequently areas such as Cambridge or Bury St. Edmunds, less than a quarter of the size of Cambridge, will surely struggle to maintain two cinemas if their offering is not substantially different, as it is now. Aberdeen is larger, but has two Cineworlds; the Commission have not instructed Cineworld as to which cinema must be sold, so customers are faced with the prospect of them retaining two Cineworld cinemas but selling a Picturehouse.

2. Why, when the OFT’s initial report (published in June) indicated that multiplex and art house cinemas operate in different markets, have these cinemas been deemed to be in sufficient levels of competition such that a substantial lessening of competition will arise?Everyone I’ve spoken to, even those who see benefit to retaining competition in these areas, recognises that these cinemas operate in different markets. Everyone except the Competition Commission.

3. Why is it believed that introducing another party to these areas will have the effect of reducing prices or maintaining them at their current levels?The only evidence that the Commission were able to provide is that the cinemas in each area monitor the prices of the cinemas of competitors. There is no evidence that they set prices competitively based on the actions of their competitors. A cursory examination of the marketplace suggests that cinema prices in each area are in a narrow range, and that competition is not as much of an influence on pricing as the local cost of living. (See my original post for sample evidence of this, looking at Cineworld prices over a wide area and also prices in Norwich which has more competition.) If the Commission wanted to be truly effectlve, they’d be looking at this issue on a national level. The likelihood is that whoever takes over each of these cinemas will offer a poorer deal for consumers, based on price and choice, and there is strong evidence to support this.

4. Why were membership schemes excluded from the final calculation as these not only create a customer loyalty to particular cinemas, but in the case of these two cinema serve to insulate their customers from price increases both locally and nationally and could act directly to negate the impact of the creation of an SLC?The Commission’s own independently commissioned research found that 58% of Picturehouse customers are members. Cineworld is also the only multiplex to offer a membership which gives direct discounts or free tickets to its members (Odeon offer a points scheme, but the rewards are significantly less), and also has abandoned booking fees online. These discounts are significantly greater than the 5% increase in ticket prices that the Commission proposed in its survey would cause customers to change cinemas.

5. Is there any evidence of any other part of the country where competition alone is successful in influencing prices? On inspection, the prices seem to be set at a level more related to the general cost of living than the factors used in the correlation in the report, and comparisons with local areas with both more competition and no competition do not suggest any evidence of a strong effect of competition on prices in this sector. The subsequent fear is that any competitor purchasing either of the cinemas will not be able to be restricted from raising prices from current levels, and I would be keen to understand the Commission’s powers to influence in this regard.Again, the focus of the Commission is very narrow, attempting to ensure competition which will do less to drive down prices than the current operators are doing at a national level. There is nothing to prevent another operator taking over the cinemas and charging whatever they want, as the Commission refuses to engage in any mechanism to control prices.

6. Given that any competing chains in both the multiplex and art house sectors are currently charging similar prices for single price tickets and less discounts to members, what controls is the Commission able to put in place to prevent a change of ownership relating in a direct increase in prices for some or all customers, which would appear to be highly likely on the available evidence?Three options exist for the purchase of each cinema: another multiplex chain, another independent chain or an independent purchaser.

- Other multiplex chains have shown a reluctance to take on small cinemas, as shown in the initial research. But the only other chain competitive on price on a national average is Empire, and they would only be competitive for customers purchasing small numbers of tickets. Any other multiplex purchaser would see an increase in prices, a loss of choice and they would be unlikely to run the other services.

- The only other independent chains are Curzon and Everyman. Neither offer the same level of diversity in their programming in their provincial cinemas as Picturehouses, and both offer less discounts to members, so the prices would rise for the majority of customers.

- Other independent cinemas in the country do manage to offer similarly diverse programming, but there would be no guarantee on prices. It must also be considered that an independent wouldn’t have the resources of one of the chains should the cinema operation encounter difficulties.

By failing to answer any of these questions, the Competition Commission have failed their duty of care to cinema customers in these three areas. The absolute best case now is that another supplier will come in and take over these cinemas, but all evidence of the industry suggests that prices of single tickets will not be any cheaper, anyone running membership schemes in other areas will offer less discounts, that choice of films is likely to go down and that there is no guarantee of support for the other services offered. The worst cases are that new suppliers fail to make the same success of these cinemas that the current suppliers have, and once the Commision is out of the picture they will each die a slow – or possibly quick – death.

I do not believe this should be the end of the fight. The Cambridge MP, Julian Huppert, has shown a willingness to continue the fight and his support is most welcome, but hopefully the 13,700 people who’ve signed the petition will also be willing to add their weight to finding a satisfactory resolution to this. I will also be contacting MPs in other affected areas today to see what support they can offer, and would encourage others to follow the same course, especially in those areas outside of the cities themselves.

Rest assured that I do not intend to give up the fight to protect what any of these cinemas offer, and the next few days will be spent attempting to secure as much support as possible for the next stages of the battle. To be clear, I still believe that losing either a Cineworld or a Picturehouse in either area results in a poorer deal for consumers and will fight to the last to protect what we currently have. If you have any views on any of the above, or wish to contribute to the battle to save any of these cinemas, please contact me at movieevangelist@btinternet.com as soon as possible. It’s still not too late to sign the petition; although this initially referred to the Competition Commission, it still acts as a focal point and a show of unified support, and the more weight we can put behind it, the better.

Thank you in advance for your support.

UPDATE: There will be a public demonstration at 17:15 on Wednesday 9th October outside the Cambridge Arts Picturehouse. If the numbers become too great, it will relocate to Parker’s Piece, almost opposite. It is hoped that Julian Huppert, MP for Cambridge, will be in attendance prior to 17:45. Please do come and show your support if you are at all able.

Cambridge Film Festival 2013: An Interview With Project Trident

![]() Cambridge film making collective Project Trident have held TRIDENTFEST, a showcase of independent film, at the Cambridge Film Festival for several years. Ahead of this year’s event, I spoke to Carl Peck about the work of Project Trident and their plans for this year’s festival.

Cambridge film making collective Project Trident have held TRIDENTFEST, a showcase of independent film, at the Cambridge Film Festival for several years. Ahead of this year’s event, I spoke to Carl Peck about the work of Project Trident and their plans for this year’s festival.

Movie Evangelist: So how long has Project Trident been running now?

Carl Peck: I think it’s six, maybe seven years. I don’t think anyone’s really sure! It came about from watching and making films here in the [Arts Picturehouse] cinema after work, often for birthdays or Halloween, and we’d make secret films to screen to people. We didn’t want anyone to know about it, so we just came up with a dumb code name and borrowed Project Trident from the nuclear weapons programme! We had enough films to make a screening, so we did a screening for our friends and called it Tridentfest. Then someone from the [Cambridge Film] Festival was at the screening and suggested screening it at the festival, and it escalated from there.

ME: As it’s evolved over the course of time, has it been difficult to fill a programme each year, or has it spurred you creatively?

CP: Bit of both I guess. We’d be making films and screening them anyway, but it does give you a bit of a kick to get things done. We used to have to ask to show films here, and now they ask us. We’re not an official selection of the film festival, but as we’re late night we have a fair amount of free rein to do whatever we want and they don’t vet the films, usually because they’re not finished in time!

ME: So, within a realm of quality you can effectively do whatever you want?

CP: We have our own internal censorship; someone will suggest something and we’re like “dude, do you really want to do that?”

ME: Is that on grounds of taste, comedy, budget or a mix of the three?

CP: It’s kind of a double edged sword, but on the other hand we’re a collective and nobody’s boss, so sometimes someone will have something weird and you just have to roll with it. But we’re pretty much all on the same wavelength.

ME: Working back from the festival each year, are you then just working on ideas to see what coalesces?

CP: Quite often it starts with a bit of messing about, for example Andrzej [Sosnowski] and Simon [Panrucker]’s films, and that will then become a story; often throwaway ideas you’d not think about, but that they make into a film. Some of my ideas come from dreams, and I have a lot of ideas in the shower, which is why I spend ages in the shower coming up with stuff. Christian’s films are usually tributes to old, trashy movies and Ryd’s into more realistic stories, which always gives us a varied mix when it comes to the finished product, and this year will be no exception.

ME: So, four days before the festival screening, how ready is it?

CP: Pretty good. I’d say it’s around 70% there, which is better than normal. It used to be a real mission as to how we’d screen films, as they’d be on DVDs and they’d always break, but now the projection is digital so we can convert the films in advance and we’re pretty sure they’re going to work. It also gives us an incentive to get them done. The rest are just finishing touches, or films like Rydian [Cook]’s. He was in New York yesterday with the world premiere of his film, and now he’s coming back to show the UK premiere with us.

ME: Has it been good for your own film making profiles?

CP: We’ve got quite a following from it over the years, but often only from people who will turn up at 11 p.m. on a Friday night. But it’s definitely been worth doing.

ME: Is there anything you’re most proud of from your years with Trident?

CP: THE PURPLE FIEND [a thirty minute short film made by the collective and shown at Tridentfest in 2011] is a highlight, but it took about two years to make. I’m really proud of the 48 hour film we made this year, for the Sci-Fi London Film Festival competition. There’s also a “making of” which Ryd’s made. [Both will be shown at this year’s TRIDENTFEST.] It was different factions coming together, and we did all the post-production in one house. We used to make films originally together, but more recently it’s been smaller groups and crossing over into each other’s teams. This was also a road test for our ability to work together and for our planning, as we’re talking about making a feature film in the future.

ME: How close were you cutting things in a two day window?

CP: We were two minutes late for the hand-in, but luckily they were quite lenient! The visual film had gone off the night before the deadline to our guy in London who does colour grading, he graded the film during the night while Simon finished off the mix of the audio. We then met up in London the next morning to put together the sound and the audio, but something in the edit had changed and so we had to get that fixed. We had something like half an hour left, and we were still in Shoreditch, frantically calling a taxi and we were running down the bridge to the BFI with this USB stick in our hands! We had a massive burrito afterwards to celebrate and then passed out.

ME: What drove you to enter the competition? Was it a chance to hone those skills?

CP: We did it a couple of years ago, and it all came together last minute, but once we’d done it you can see what’s involved in achieving that. We had a real structured plan this time of how to operate. You can’t prepare as such but you’re allowed to source locations, costumes and things like that. We’d managed to get a cool location in an airfield, and took a bag of clothes, military stuff that would look good in a sci-fi film. We were there while the brief was being picked up in London. We then gave ourselves around two hours to script, shot it all, then got back to Cambridge at ten o’clock that night and gave the footage to Alex who edited it overnight, then got up in the morning and worked on the post – sound, music, visual effects, and then shot some pick-ups on the roof of the house we were in. Some shots we didn’t have so we just animated them, I don’t think you’d ever notice.

Each room was a different studio. Simon’s bedroom was a sound studio, he had his bed turned upside down, in one room we had our edit and in the kitchen was visual effects and Rydian was making the Making Of [documentary] while it was happening – hence it’s not finished! It looks great on the big screen. We showed it last week to West Suffolk College as they’re also entering their own 48 hour competition.

ME: And has that also become part of the work of Trident, of inspiring and helping other film makers?

CP: Yes, that’s always been our thing, to try to spread the message that there’s no reason you can’t make films if you want to. If you’ve got an iPhone, you can make a film.

ME: We now live in the YouTube generation. How much difference is there between picking up an iPhone and the process you’ve gone through for the competition?

CP: We didn’t start doing that, you don’t need all that to start with but we’ve progressed since we started and are now getting people involved and the team’s grown so we can do that sort of stuff. There’s always someone out there who’s in a band and you can ask if you can use his music. You’d think you couldn’t make a film, but the more people you ask the more it escalates.

ME: Music videos have also been a feature in previous years, is that something that’s happening this year as well?

CP: I think I said last year that I wasn’t going to do any more for free, and the one film I have this year is a music video! The one I’m doing is with a rapper from Peterborough who’s a really nice guy who was featured on Radio 1 Xtra recently.

ME: What are the highlights of this year’s programme?

CP: We have fourteen films on the list this year. We have some of Simon’s crazy films he’s been making in Bristol, the return of Simon and Andrzej’s Poo Brothers films, three new ones from them, a really trippy one called Brian. There’s also one file in projection that no-one’s heard of – who knows what that’s going to be? It usually comes together on the night, you never know if anything isn’t going to be ready or broken, so even if we haven’t collectively seen them we know what they’re about and we can loosely gauge the vibe. We’ll also have some news about our future plans, which hopefully include a feature film.

ME: Carl Peck, thank you very much.

Tridentfest 2013 screens Friday 27th September at 23:00 at the Cambridge Arts Picturehouse, and tickets are available via the usual box office routes.

The Half Dozen: 6 Most Interesting Looking Trailers For September 2013

Okay then, So this time last month, I was posting up a list of my six trailers for August, and was merely a humble blogger. One month later and I appear to be well on the way to a full-blown activist and campaigner. In case you missed it (and if you did – WHERE WERE YOU?!), the Competition Commission announced plans to compel CIneworld group to sell either Cineworlds or Picturehouses near to where I live, I wrote a 5,000 word rant spread over two days based on the fallacy of the decision as I perceived it, and then went on to start a petition that’s had 12,000 signatures in a couple of weeks (thanks to the efforts of all those valiantly spreading the word on its behalf). You could say it’s been an interesting month.

But I believe in fighting for what’s important in life, and to me cinema has become one of my great loves over the past few years. Even with the cinemas close to me, it’s difficult to find all of the films on offer; a rifle through any of the main film publications of our time will list reviews of films on release anywhere in the country, but actually tracking down showings of these can sometimes prove troublesome. I’ve got twenty-five multiplex screens and five art house screens within half an hour’s drive, and they show a wide variety of films, but even they can’t manage to get everything when the multiplexes are replicating their content so heavily.

So this month I’ve picked out six films that anyone picking up a copy of Empire or Total Film might read the review of and think of popping to their local cinemaplex to catch, but in my case each would require a one way trip of the length outlined below just to catch the film. (I have made trips of this length before on occasion, but with the Cambridge Film Festival just a week away I’m going to be sticking a little closer to home for now.)

No One Lives

Nearest showing: Leicester Square

Travel time: 1 hour 29 minutes

Any Day Now

Nearest showing: Dalston

Travel time: 1 hour 20 minutes

42

Nearest showing: Enfield

Travel time: 1 hour 12 minutes

Museum Hours

Nearest showing: Ipswich

Travel time: 55 minutes

In A World…

Nearest showing: Stevenage

Travel time: 55 minutes

Pieta

Nearest showing: Ipswich

Travel time: 55 minutes

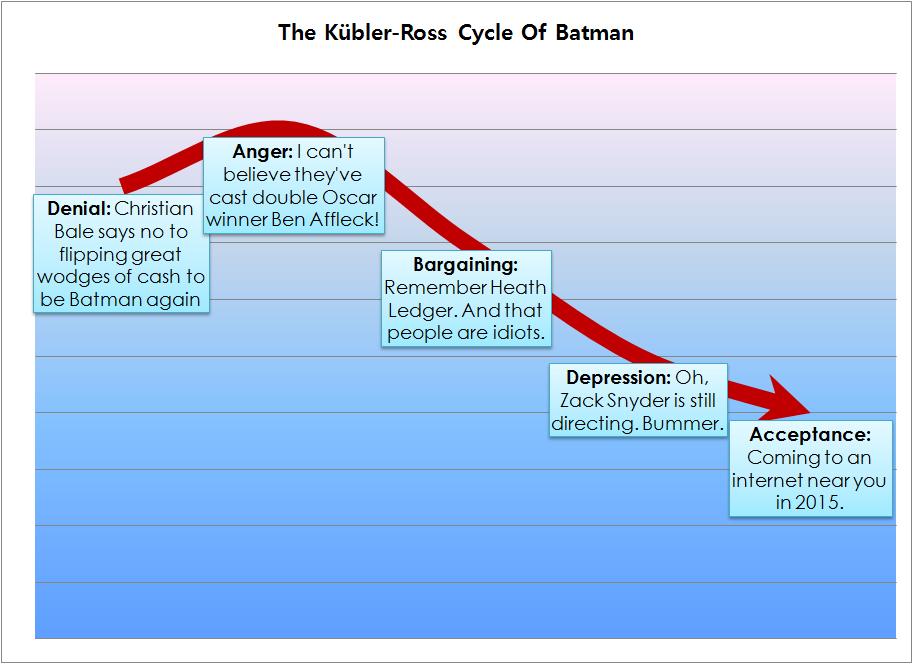

The Kübler-Ross Cycle Of Batman

Ben Affleck will be appearing in numerous supercuts of people saying “I’m Batman” in around 2 years. In case you hadn’t heard.

Ben Affleck will be appearing in numerous supercuts of people saying “I’m Batman” in around 2 years. In case you hadn’t heard.

The Cineworld / Picturehouse Competition Commision: Brief Thoughts On The Full Report

Following my post yesterday regarding my thoughts on the initial findings of the Competition Commission’s review into the purchase of City Screen Limited and the Picturehouse chain by Cineworld Group plc, the commission have now published their full findings into the purchase which support their recommendation that one of the two arms of the new business should be required to sell their holdings in Aberdeen, Bury St. Edmunds and Cambridge in order to offset the impact of the substantial lessening of competition (SLC) created by the purchase.

I will now, briefly, give my thoughts on the four questions I posed at the end of my initial report and what I’ve learned from an initial scan through the fuller findings. I am likely to come back to update this as the findings plus appendices run to over 240 pages, and I have a full time job and both a trip to FrightFest and hosting a Q & A at one of the affected cinemas to prepare for at the weekend (yet another example of an activity and a benefit to the public that may be potentially lost if it was the Picturehouse arm to be sacrificed). However, both the publication of the report and the following discussion, of which I have been but a small part, seem to have prompted strong emotions and so I wanted to take an initial opportunity to reflect on the fuller report and to see if we could better understand the findings.

The other thing I would say at this juncture is that I fear there’s a risk I may be seen to be working to protect the commercial interests of a public limited company. I have no shareholder interest in the company, and my most direct involvement is to take part in events organised in its cinemas. (I will have been involved in Q & As at both Cambridge Arts and Abbeygate Picturehouses this year, and I give up my time voluntarily to watch screeners and to prepare for these sessions, as do a whole host of other people. The cinemas are also not charging a premium for these events.) I believe that it is right that we have an independent body seeking to protect consumers from damaging changes to their interests, but that any proposals need to be measured from a quality as well as a cost perspective. I would also add that I would love to see a growth in both areas of competition and especially of more independent cinema, especially in those areas outside the city and town centres referred to, but this doesn’t appear to be within the scope of the current report.

Anyway, to the questions, and my thoughts on where we might go next.

1. Why is competition a requirement in areas such as Cambridge and Bury St. Edmunds, when geographical areas of similar size do not typically have such competition?

The report and its findings have done a very thorough job into examining the surrounding competition, but there seems to be no setting of a particular requirement for competition in a given area. This is potentially more of a problem for Bury St. Edmunds than it is for Aberdeen or Cambridge, as it represents a removal of competition rather than an a reduction. Analysing the results of the regression analysis in the report is also somewhat difficult as confidential information has had to be removed, but the key statistic would seem to be that there are mean of 1.8 fascias (cinemas) within the 20 minute radius defined as suitable travel time of Cineworlds outside London, and 2 for Picturehouses, if in both cases you exclude small cinemas. However, the report has not considered these ratios or statistics for any other chains, or what the prevailing market conditions should be.

What I’ve also not yet been able to find in the report – and please feel free to guide me to this if I’ve missed it – is any analysis as to whether competition in the market is having an effect on prices over the course of time, i.e. did the period prior to the acquisition see prices fluctuate or change thanks to the benefit of competition? There is a large amount of anecdotal evidence provided that the cinemas monitor the prices of other cinemas in the surrounding area, but I cannot then see any connection to those cinemas adjusting prices. I would be keen to understand the effects of this both in the markets under scrutiny and those such as Norwich which have high levels of competition among other chains, but where at present competition doesn’t appear to be doing much at face value to impact on prices.

2. Why are the Cineworld and Picturehouse chains being deemed to be in competition when Picturehouses are generally complementing the offering in other areas rather than challenging it, and when the Commission’s own findings demonstrate that these are appealing to different demographics, have little overlap in terms of content, and the Picturehouse has an appreciably different experience surrounding the exhibition?

I have been able to find reference in the report to the overlap in terms of revenue, which at the Bury St. Edmunds cinemas is listed at 26%. However, I believe this hasn’t truly grasped the nature of the offerings of the Picturehouse cinemas. There is a statistical principle known as the pareto principle, or in layman’s terms the 80-20 rule. This states that typically, 80% of the effects come from 20% of the causes. It is likely that a small number of the showings at the Picturehouses, coinciding largely with those that overlap with the other multiplexes, represent the larger proportion of their revenue. But in my analysis, the Cambridge Cineworld is showing 22 films in a 10 day period over 9 screens – that’s an average of 2.33 films per screen. The Cambridge Arts Picturehouse is showing 21 films and events in the same period over 3 screens, an average of 7 films per screen, and the Abbeygate in Bury has a similar ratio. It is that diversity that its patrons are keen to protect, and the report in prioritising revenue as a deciding factor in customer decision making has neglected to examine the effect of, or on, consumer choice within the programming of each cinema.

The local market also needs to be taken into account, and by that I mean the number of available screens. In my extensive experience, the Picturehouses in Cambridge and Bury have some of the most diverse programming of the Picturehouse chain. There are a reasonable number of films that I would be able to watch at larger Cineworlds such as Stevenage (16 screens) or Enfield (15) or those nearer to London in a more competitive market such as West India Quay (10 screens, but with much less overlap of programming with Cineworlds in Cambridge or Bury). The Cineworlds in Cambridge and Bury have only nine and eight screens respectively, and this has driven a market condition where the programming is being driven to be more diverse by the requirement for greater consumer choice. The implications of the removal of either of these chains from the local market would need to be carefully considered, as I would have presumed it unlikely that any prospective buyer would be able to increase the screen counts of any of the cinemas.

If the Picturehouse were to be forced to be sold, the two competitors offering the most similar programming across their chains are the Curzon and Everyman cinema chains. Curzon has recently opened its first cinema outside London, increasing its portfolio to six, while Everyman has ten cinemas, four in Surrey and Hampshire and one in Leeds, and both offer similar membership schemes to the Picturehouse chain. All of the cinemas outside London struggle to offer such a high film to screen ratio as the Cambridge and Bury Picturehouses, and any prospective purchasers would not only need to demonstrate an ability to significantly step up their ratios in terms of content, but also their willingness to support the cinema culture, at events such as the Cambridge FIlm Festival which operates extensively at the Picturehouse (and has occasionally in previous years had second screenings at the Cineworld as well). Others more knowledgeable than I would be able to greatly extend the list of other activities taking place in these areas that have grown organically out of the current operations and may be at risk if ownership changed.

All of this seems to have glossed over the initial statement by Cineworld, unchallenged by anyone as far as I can see, that it acquired the Picturehouse chain to gain entry to a segment of the market it wasn’t currently operating in. On that basis, I am struggling to see how the two chains could have seen to be in competition, otherwise there would have been no value to the purchase.

3. Why would introducing an additional party to these areas drive competition in prices when there is no evidence to support this, and when pricing seems to be driven as much by the local cost of living as by any perceived competition?

The report hasn’t answered the question that adding a competitor would increase competition, only that by removing a competitor there is an SLC created. The key new piece of evidence appears to be the mathematics used to draw that conclusion. The Commission have used a gross upward pricing pressure index (GUPPI) to examine the likely impact of the loss of competition, and concluded that the Picturehouse cinemas would be most likely to benefit based on the potential diversion of custom and the respective unit margins on each ticket price. This, I presume, means that the Picturehouse becomes most at risk of being sold off, even though it is in less direct competition with its near neighbour. What this calculation is based on is the standard adult ticket price. There appear to have been reviews made for concessions and for special events, but membership appears to have been excluded – both from the cost of membership, as it doesn’t relate to one-off ticket prices, and it’s impact on individual sales – and when the two cinema chains offer the two most beneficial membership schemes in the industry.

The other calculation that has been used is a regression calculation to assess the pricing, correlated against two key variables: the concentration and controls. Again, the concentration is related to the number of fascias (cinemas), rather than the number of screens or the potential programming, and the controls were the local unemployment rate, the average hourly wage and the proportion of customers under 35. However, what we cannot see is the closeness or fit of the correlation produced by this analysis, so we cannot determine how significant these respective factors have been. I still believe that the cost of living has more impact on current pricing nationally than local competition, and believe that there is much more that could and should have been done to test this hypothesis.

4. Why would allowing another major operator to take over these chains be in the interests of consumers, when the price difference for casual attendance is negligible and for regular attendance is either similar or significantly cheaper?

I think I covered this yesterday, but let me reiterate – the report has covered the possibility of the creation of SLCs, and concluded they will occur in three markets. They have only been able to propose one solution, and that solution for the removal of the Cineworld would see negligible price changes for casual attendance and marked increases for regular attendees. I didn’t cover the membership schemes of the Picturehouse rivals yesterday, but to address that, both other chains offer membership schemes at similar prices for the annual outlay. However, at those price points Picturehouse give three free tickets a year and the others two; Picturehouse also discount other events by up to £2 a ticket, whereas it’s £1 at Everyman and there is no discount at Curzon. The one offering which Picturehouses don’t give is an annual flat rate membership, costing £600 for Everyman (or seeing nearly as many films as I do to get the benefit), or a very reasonable £300 for the Curzon. This equates to around 25 films a year at West End prices, and at Cambridge prices would be around 30 films, so for those seeing 3 films or more a month, a price point such as this would start to give Curzon the edge. However, the price rises to £500 if you wish to include non-cinema events and they do not currently offer anything than a one-off payment option, which would likely put such a charge out of the range of many.

The commission also surveyed a number of customers by both e-mail and telephone, making the two sets mutually exclusive, but there is also some doubt in my mind as to whether those surveyed fully understood the questions being asked. The price rise question was posed in terms of a 5% increase, but if this concern had been expressed in real terms – i.e.. 40 – 50 pence per ticket – would it have generated the same magnitude of proposed response? Also, were respondents aware that their alternate cinema showed only a maximum of 18% of similar films by content and 26% by revenue, thus limiting their options to switch anyway?

But the key for me on this last point is the lack of a suitable alternative. Whatever the pros and cons of the original decision, there has been no direct consideration by the Commission on the possible effects of their one solution, and no matter which chain is sold I can see nothing but an adverse effect on price, choice or both. We desperately need a solution which will protect the interests of consumers for both cost and diversity but still promote free market competition – any ideas extremely welcome. Don’t forget to continue to voice your thoughts to the Commission or to your local MP (links at the bottom of yesterday’s article).

The Cineworld / Picturehouse Competition Commission Decision: My Interim Findings

In the three and a half years I’ve been blogging, that may be the most serious blog title I’ve ever written. But suddenly we are living in serious times, with a threat to the cinematic options of thousands of people being presented today by the initial findings of a Competition Commission investigation into the purchase by Cineworld Group plc last year of City Screen Limited, the group which operates the Picturehouse chain across the UK.

I believe I stand a chance of being the single individual to be most affected by this decision, but I would be far from the only person to suffer if these changes are forced through. Since I moved to the area in 2007, I have made around 750 trips to the cinema, of which over three quarters have been to four local cinemas. I live twenty-five minutes from Bury St. Edmunds, where I am a regular at both the Cineworld and the Abbeygate Picturehouse, and thirty minutes in the other direction is Cambridge, where I occasionally visit the Vue cinema, but more regularly the Cineworld and the Arts Picturehouse. Today the Competition Commission announced their initial findings into an investigation they started in April, and their recommendation to prevent the adverse effects that could be created by the merger is to sell off one of the two cinema chains in three affected towns and cities: Aberdeen, Cambridge and Bury St. Edmunds. That means that either the Picturehouse or the Cineworld would be no more in those three areas.

Reading the documentation is a strange descent into legalese, which I would presume most people (myself included) would only encounter in the event of a house purchase or making a will. The key paragraph from the initial findings is this:

“…the creation of that situation has resulted, or may be expected to result, in a substantial lessening of competition (SLC) in the market for cinema exhibition services in the Aberdeen, Bury St Edmunds and Cambridge areas.”

So there is no requirement on the commission to prove an SLC, just that one may occur. This seems oddly arbitrary, but I’m not here to question the workings of the process. The Commission is, in case you weren’t aware (taken from their own website):

“…an independent public body which helps to ensure healthy competition between companies in the UK for the ultimate benefit of consumers and the economy. It conducts in-depth investigations into mergers and markets and also has certain functions with regard to the major regulated industries.”

I am happy to trust implicitly that the commission is not politically motivated, but my instincts are telling me that I cannot see who is well served by the prospects of the sale of these cinemas. From a personal perspective, either would be catastrophic. I have a membership with Cineworld which gives me free tickets and discounted concessions, and an average travel time to my two nearest cinemas of 27 minutes. If the Cineworlds were sold off, then my nearest two venues become Huntingdon (40 minutes) and Haverhill (50 minutes), increasing my journey times by 60%. I see an average of eight films a month at Cineworld and simply couldn’t afford to do that without Cineworld’s Unlimited scheme – no other chain or independent operates a similar scheme. For the Picturehouses, my nearest alternatives would be Norwich, Hackney or Stratford (all over an hour away), and suddenly independent cinema would be reduced from four films a month to probably one a quarter.

But I would be the first to admit that I am not at the centre of the bell curve in terms of cinema attendance, instead very much in the top quintile (possibly the top percentile). So in an effort to understand the fairness and implications of the Commission’s decision, I’ve looked at a number of key areas for a more average cinema attendance to see if their findings stack up. (I’m leaving out Aberdeen from my comparison as it’s not local to me, but many of these points may also apply.)

Comparable demographics

The first point I’d like to consider is what constitutes sufficient competition. If you look at the definition within the findings, the Commission has considered an area thus:

“For the geographic market definition, we established the boundaries of the markets based on 20-minute isochrones around the parties’ cinemas, but we recognized the need to apply this rule flexibly when assessing competition in specific local areas.”

Or in other words, it considers a twenty minute journey to be the reasonable upper limit for times to reach each cinema for these purposes.

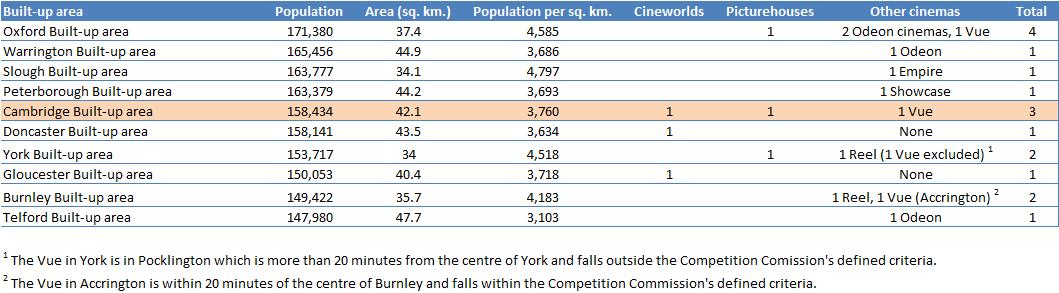

I’ve compared Cambridge with a number of similar sized areas. If you consider the urban areas defined in the 2011 UK census, then of the nine others most similar in size to Cambridge, only three other built up areas have more than one cinema. Oxford is particularly blessed, having three other major cinemas in addition to its Picturehouse, but the median average of this sample is 1. Since the average cinema for this sort of area is 1, it seems likely that the average population of areas of similar size to Cambridge can typically only support one cinema, unless there is some other factor in the diversity of those cinemas. (Since Bury St. Edmunds has a population of only c. 35,000, it clearly falls into the same category, so can be considered fortunate to retain two cinemas at present.)

In this table, Burnley is a slight oddity in that a cinema in another town is just within geographic reach. However, in the other three cases, those areas of similar size that can sustain an additional cinema – York, Oxford and Cambridge – all count a Picturehouse as one of their cinemas. These were all Picturehouses well established prior to the purchase of City Screen limited, suggesting a public demand for what the Picturehouse cinemas have to offer.

When considering the services offered by City Screen Limited, the Commission also considered the distribution services offered by the company. With reference to this point, they observed:

“…we found that Picturehouse’s programming services are advisory and customers typically make the ultimate programming decisions.”

This would seem to support that, in these areas, customers are seeking the offerings made by the cinemas, and that in areas that can support more than a single cinema that is only possibly because customers are seeking a more diverse offering.

Consumer choice and the question of direct competition

If you compare the programming lists for a ten day period at both Cineworld and Picturehouse in Cambridge and Bury St. Edmunds, that diversity shows through very clearly:

In that 10 day period (Tuesday 20th – Thursday 30th August 2013), both Cineworlds are showing 22 different films. Only 9% of those films are also showing at the Picturehouse in Cambridge, and although the Bury figure is higher, it’s only 18%. These are clearly two different cinemas offering to two different demographics, and these programming choices are being dictated by consumers. There are a couple of films showing at the Cambridge Arts Picturehouse that previously ran at the corresponding Cineworld, but this would just demonstrate the advantage of two cinemas allowing a longer run for films that appeal to a particular audience. If one or other chain were forced to pull out of this area, then the variety would be significantly diminished and consumer choice reduced.

In that 10 day period (Tuesday 20th – Thursday 30th August 2013), both Cineworlds are showing 22 different films. Only 9% of those films are also showing at the Picturehouse in Cambridge, and although the Bury figure is higher, it’s only 18%. These are clearly two different cinemas offering to two different demographics, and these programming choices are being dictated by consumers. There are a couple of films showing at the Cambridge Arts Picturehouse that previously ran at the corresponding Cineworld, but this would just demonstrate the advantage of two cinemas allowing a longer run for films that appeal to a particular audience. If one or other chain were forced to pull out of this area, then the variety would be significantly diminished and consumer choice reduced.

Which makes it difficult to understand how these cinemas can be seen to be in competition. This is all the more baffling in light of two statements in the Commission’s findings. Firstly, this set of comments:

“Cinemas are of various sizes, and a distinction is generally made by the industry between multiplexes (which have more than five screens) and other cinemas.”

So the commission recognises that the industry itself differentiates at a basic level between the kind of cinemas represented by Cineworld and its direct competitors, and that of the Picturehouse chain. The Arts Picturehouse has three screens and the Abbeygate two, so there is a clear divide between the two arms of the new business. The statement continues:

“Operators of multiplexes tend to focus on showing mainstream films and to offer a largely undifferentiated service… Operators of smaller cinemas, which are generally located in town and city centres, may differentiate themselves from multiplex operators not only through the location of their cinemas and the mix of films they show (which will generally include both mainstream and specialized films), but also through the ancillary services and general ambience their cinemas offer to their customers.”

So there is a recognition here that not only do the Picturehouse cinemas offer a different cinematic experience to that of the standard multiplex, but also a different cultural experience. Both Picturehouses have a bar, offering hot and cold food and a selection of alcoholic beverages which can be taken into screenings.

However, having clearly established this differentiation in market and offering, the Commission inexplicaby – as in no explanation for this decision is given in the document – then decides to disregard its own differentiation in coming to a decision.

“We defined the relevant product market as the market for the provision of cinema exhibition services, and we saw no reason to include within the definition of the relevant product market other leisure activities and/or food and beverages.”

I have attended eleven Cineworlds and four Picturehouses in the last two years, and while a few Cineworlds offer an on-site bar, they typically don’t then allow alcohol or other foodstuffs purchased outside of the concessions stands to be taken into screenings. What I can testify to is that in general, a Cineworld is very comparable in terms of exhibition and concessions to the other major chains (Odeon, Vue, Showcase, Empire and Reel, as I have attended cinemas in all of their chains in the past three years), whereas the Picturehouse is a markedly different experience. No reasonable definition of what the cinemas are offering can disassociate the wider experience from the exhibition, and I would urge the Commission to reconsider this point. Visiting the cinemas themselves may offer additional insight into this point, if they have not yet done so (and no indication is given that they have).

The only other differentiation that I can find that relates to the findings is that where most multiplexes are defined as out of town, the three Cineworlds in question – Aberdeen, Cambridge and Bury St. Edmunds – are all effectively in town and within walking distance of their competition. The Commission gives no direct indication that this has been a factor in their decision.

The effect of a potential purchase and competitive pricing

Within the Commission’s findings, there is one key paragraph that outlines the potential impact of an SLC (substantial lessening of competition) that the decision to recommend a sale of cinemas seems to hinge on, having ruled out any possible impacts from planned expansion of either chain or from City Screen Limited’s distribution role:

“…may be expected to result in a substantial lessening of competition (SLC) in the markets for cinema exhibition services in the Aberdeen, Bury St Edmunds and Cambridge areas, leading to adverse effects, for example in the form of higher ticket prices than would be the case absent the merger.”

According to the BFI Statistical Yearbook 2011, in that year 62% of the UK population visited the cinema at least once a year, and 19% at least once a month. Let’s now consider the potential effect of a sale on the pricing for the cinemas in question for these two groups of people.

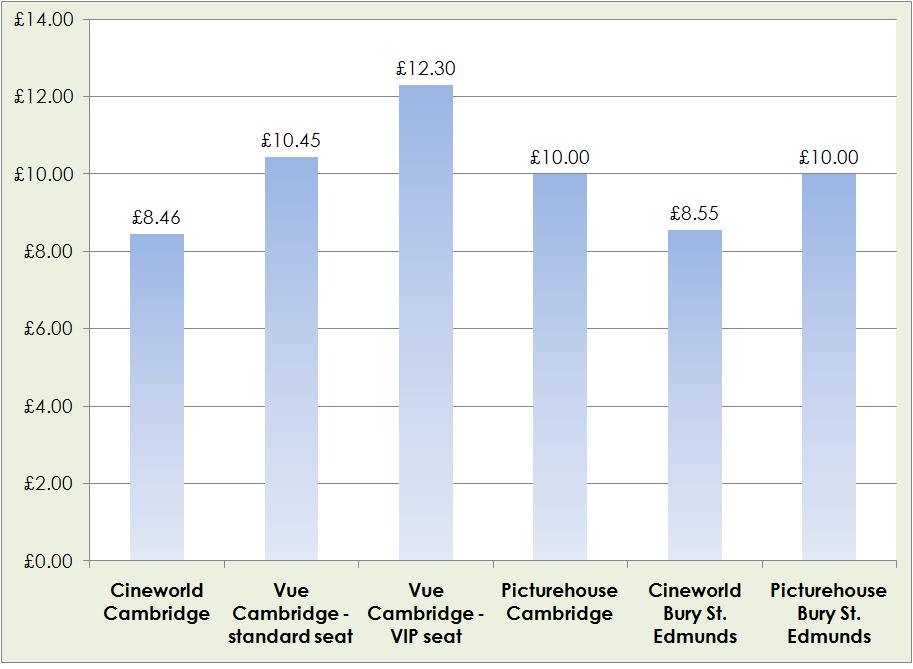

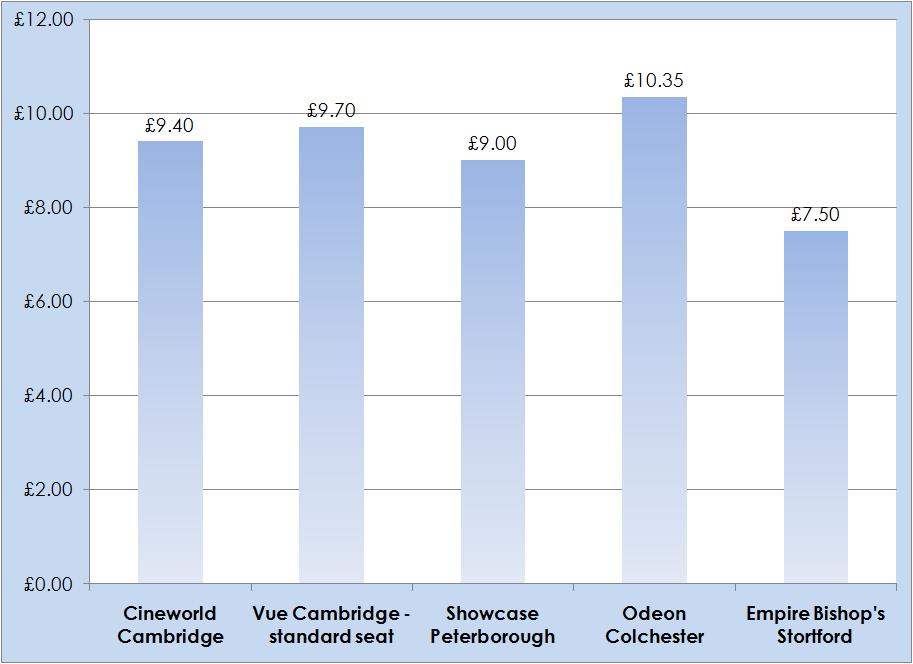

Firstly, let’s consider the financial the group that visits once a year or more. That group is making irregular purchases, so is most likely to notice the effect of a change in a single price ticket. Let’s firstly compare the prices of a ticket for the main cinemas in both Cambridge and Bury St. Edmumds. The price shown is that for a single adult ticket purchased on arrival at the cinema for a showing this coming Friday evening (23rd August 2013) – it should be noted that all three chains offer concessions and have a day with reduced ticket prices for all customers, and there are similar differentials in price for those options.

So if you compare the standard price ticket at Cineworld to that of the area’s main competitor, Vue, then the prices are favourable, and the Picturehouse seats are cheaper than a standard ticket at the Vue in Cambridge, even though I would argue that it’s not a direct comparison due to the programming point made earlier (the Vue is also showing 22 films in the ten day period, all of which are showing at one of its competitors with the exception of a single afternoon screening for seniors).

So if you compare the standard price ticket at Cineworld to that of the area’s main competitor, Vue, then the prices are favourable, and the Picturehouse seats are cheaper than a standard ticket at the Vue in Cambridge, even though I would argue that it’s not a direct comparison due to the programming point made earlier (the Vue is also showing 22 films in the ten day period, all of which are showing at one of its competitors with the exception of a single afternoon screening for seniors).

There is an even more marked difference if you compare the prices for tickets purchased online. Cineworld offer a national scheme called myCineworld, which is free and has no commitment to the number tickets purchased, and offers a 10% reduction and no booking fee. The Picturehouse chain also do not charge a booking fee in any of their cinemas for tickets purchased online, but Vue charge a 75p online booking fee. So the online comparison becomes:

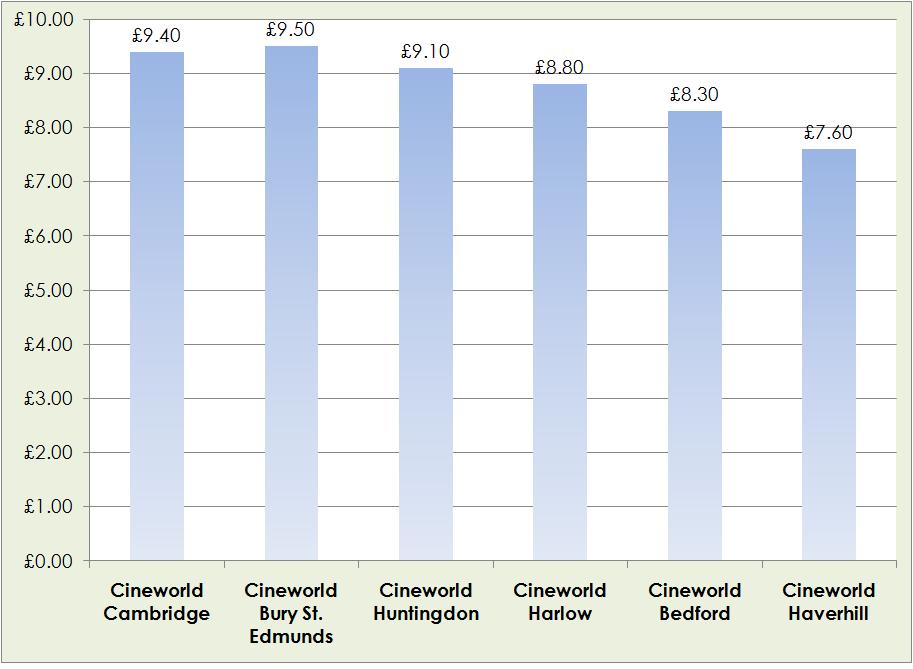

So while the cinemas under threat are currently undercutting their direct competitor in the Cambridge market, the argument made by the Commission is that the market conditions and the reduction of competition will drive higher prices. At face value, there may appear to be some weight to that argument, if you compare the prices of these two Cineworlds to other cinemas in the chain within a reasonable distance.

So while the cinemas under threat are currently undercutting their direct competitor in the Cambridge market, the argument made by the Commission is that the market conditions and the reduction of competition will drive higher prices. At face value, there may appear to be some weight to that argument, if you compare the prices of these two Cineworlds to other cinemas in the chain within a reasonable distance.

However, the Commission is proposing that the lack of competition will drive prices up, and in each of those other areas there is no competition, the Cineworld being the only cinema in the area. This would seem to argue against that effect.

However, the Commission is proposing that the lack of competition will drive prices up, and in each of those other areas there is no competition, the Cineworld being the only cinema in the area. This would seem to argue against that effect.

Next, let’s consider the East Anglian cousin of Cambridge and Bury St. Edmunds, Norwich. There are four cinemas in Norwich, all of which are in the city centre and would fall within the conditions that the Commission have laid out. The Picturehouse here has similar programming to Cambridge and Bury, while the other three are all offering standard multiplex fare. The Friday night price for each of these is as follows.

There is a key observation to be made from these prices. Although the Vue seat here is cheaper than its comparable seat in Cambridge, the most expensive seat in the area is the same price range as a higher priced seat in Cambridge or Bury. Additionally, a significantly cheaper competitor in the form of the Hollywood appears to be having no effect in driving prices down in the others.

There is a key observation to be made from these prices. Although the Vue seat here is cheaper than its comparable seat in Cambridge, the most expensive seat in the area is the same price range as a higher priced seat in Cambridge or Bury. Additionally, a significantly cheaper competitor in the form of the Hollywood appears to be having no effect in driving prices down in the others.

This would suggest that forces other than local competition are having an effect on price. One other possible reason for the higher prices in Cambridge (and by extension Bury St. Edmunds, which is only 35 minutes away by car) is the cost of living in the area. In this 2012 survey on house prices in the UK, Cambridge is shown to be the sixth most expensive in the UK. I would propose that the higher cost of living in the area is also having an effect on ticket prices. I would like to see what research the Commission has done into investigating or eliminating other factors in terms of the setting of ticket prices in these cinemas.

Finally on the single ticket, we must consider the alternatives. Three other major chains operate in the south of England: Odeon, Showcase and Empire. Presuming that there would be no advantage to Vue purchasing one of the Cambridge cinemas, compare the prices of the nearest geographical cinemas in each of the other chains. It should be noted that, in each case, the cinema is the only one within a geographical area of the size stipulated by the commission.

Finally on the single ticket, we must consider the alternatives. Three other major chains operate in the south of England: Odeon, Showcase and Empire. Presuming that there would be no advantage to Vue purchasing one of the Cambridge cinemas, compare the prices of the nearest geographical cinemas in each of the other chains. It should be noted that, in each case, the cinema is the only one within a geographical area of the size stipulated by the commission.

Again, there is a wide variety of prices here, with no guarantee on this evidence that if one of these chains took over a cinema in question that it would cause the local market to become more competitive.

Again, there is a wide variety of prices here, with no guarantee on this evidence that if one of these chains took over a cinema in question that it would cause the local market to become more competitive.

When all things are considered, the price range across all of these tickets is between £7 and £10. I would also like to see evidence from the Commission that those attending the cinema infrequently would be likely to be swayed in their decision by such small price differentials, as such differences may become negligible when factoring in other costs of attending the cinema such as the concessions, travel and parking.

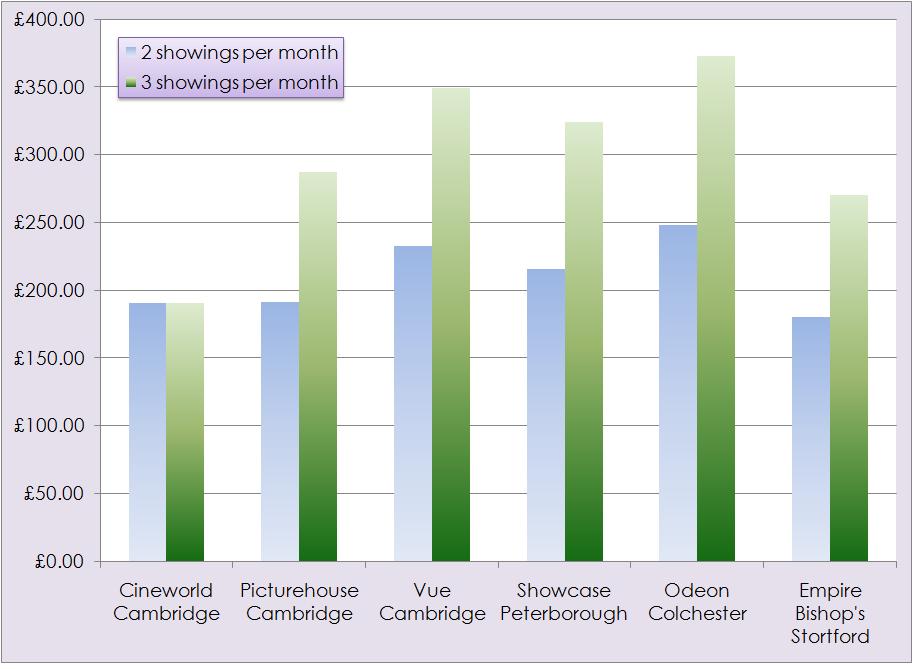

The second consideration is for those attending the cinema more regularly. Two chains in the UK offer national membership schemes for their patrons which offer significant discounts for members, both valid at any cinemas outside of the West End for the rate that would be paid in Cambridge or Bury St. Edmunds. The Cineworld scheme costs £15.90 per month and entitles the holder to attend an unlimited number of screenings, while the Picturehouse charges an annual fee of £35, offers three complementary tickets and then reductions of typically £2 per screening on any further tickets bought. Both chains also offer money off concessions; Cineworld discounts include 25% off for members staying longer than 12 months, and Picturehouse’s 10% discount applies to all bar purchases, including food and alcohol.

The BFI survey indicated that 19%, or around a third of all people who attend the cinema, attend at least once a month. So let’s compare the costs of attending two or three weekend screenings per month across each of the major chains, including the cost of purchasing any memberships.

At two showings per month, the Cineworld and Picturehouse chains are cheaper than anyone except the Empire, who are only £10 cheaper per year. Once the figure rises to three, then the Cineworld becomes the cheapest option, and with no restrictions on further attendances.

At two showings per month, the Cineworld and Picturehouse chains are cheaper than anyone except the Empire, who are only £10 cheaper per year. Once the figure rises to three, then the Cineworld becomes the cheapest option, and with no restrictions on further attendances.

I believe, in the light of this, there are a number of questions that need to be answered before further action is taken.

-

Why is competition a requirement in areas such as Cambridge and Bury St. Edmunds, when geographical areas of similar size do not typically have such competition?

-

Why are the Cineworld and Picturehouse chains being deemed to be in competition when Picturehouses are generally complementing the offering in other areas rather than challenging it, and when the Commission’s own findings demonstrate that these are appealing to different demographics, have little overlap in terms of content, and the Picturehouse has an appreciably different experience surrounding the exhibition?

-

Why would introducing an additional party to these areas drive competition in prices when there is no evidence to support this, and when pricing seems to be driven as much by the local cost of living as by any perceived competition?

-

Why would allowing another major operator to take over these chains be in the interests of consumers, when the price difference for casual attendance is negligible and for regular attendance is either similar or significantly cheaper?

You can find a copy of all of the commission’s initial findings here. If you feel strongly about this, I would urge you to make your feelings known, both to the Commission at cineworldcityscreen@cc.gsi.gov.uk before September 10th and to your local MP, Julian Huppert for Cambridge and David Ruffley for Bury St. Edmunds. Thank you for listening.

The Half Dozen: 6 Most Interesting Looking Trailers For August 2013

The passing of another month, and it’s been a hot July in the UK, which is never good news for cinema attendance. I’m gingerish, so will do a definitive boiled lobster impersonation if left in the sun for more than around 20 minutes, but part of my cinema philosophy involves seeing films in the company of others, so I’m hoping for both self-interest and selfish reasons that the heatwave doesn’t maintain too much longer.

Especially because the list of films due out in August is so promising, nestling as it does between the back end of summer blockbuster season and the start of the festival season in September. I do take my time over this list every month, perusing the upcoming lists of films at the Internet Movie Database, Rotten Tomatoes and Launching FIlms among others to try to find the cream of what’s coming up. So in an average month for preparing this post I typically watch all or part of around 30 trailers to attempt to whittle this down to the six best.

That’s been as tricky as ever this month, so to shake up the format a little I’ve first narrowed it down to a dozen, and then paired them off in some tenuous themes for a head-to-head battle to the death. I’ve included the trailers for both, so feel free to tell me if I’ve got any of these face-offs wrong. (It also means I have an excuse to skip the trailer for Only God Forgives, as (a) there’s nothing else like it coming out, and (b) it was in last month’s rest of the year preview.)

LET BATTLE COMMENCE! (Sorry, got a bit carried away there.)

The Well Regarded Horror Movie Face-Off: The Conjuring vs. You’re Next

Since the demise of the late, much lamented Empire magazine event in August, variously called Movie-Con or Big Screen, I have instead spent my pennies on a day at Film 4 FrightFest. Last year threw up a right mix, from the sublimely twisted (Maniac) to the unintentionally ridiculous (Tulpa), and for those attending the opening night, they’ll be treated to You’re Next as their final film. I’ve got R.I.P.D to “look forward to” in my six film on the Saturday, so if you’re around at the Empire Leicester Square on the 24th, do say hi. (Warn me on Twitter first so I know you’re coming.) But of the mainstream horror releases, these two look to be the pick of the crop this month. I’ve always been a fan of harder shocks and gore (hence buying a ticket for FrightFest), so only one winner in this category.

WINNER: You’re Next

The Funny / Serious Steve Coogan Face-Off: Alan Partridge: Alpha Papa vs. What Maisie Knew

Steve Coogan once did a live show called “Alan Partridge and Other Less Successful Characters”, and that might sum up the permanently typecasting effect that being Norfolk’s premier fake celebrity has had on Steve Coogan’s career. But in a month where a man who’s given us the likes of “He must have a foot like a traction engine!” and “Dan! Dan! Dan! Dan! DAN! DAN!… DAN!… DAN!” has a film out there can only be one winner.

WINNER: Alan Partridge: Alpha Papa

The Almost Inevitably Disappointing Follow-Up Face-Off: Kick-Ass 2 vs. Elysium

I thought that both Matthew Vaughn’s Kick-Ass and Neill Blomkamp’s District 9 were outstanding of their examples of their genres, neither quite as ground-breaking as they seemed at the time, but both thought provoking pieces of high quality entertainment. Vaughn has passed the torch to Jeff Wadlow on the Kick-Ass sequel, while Blomkamp looks to be revisiting a little of the same ground with his sophomore feature film. Both will inevitably disappoint slightly in regard to their predecessors, but which one will suck slightly less?

WINNER: Elysium

The Sharp Indie Comedy Looking To Avoid The Summer Blockbusters Face-Off: The Kings Of Summer vs The Way, Way Back

August is so packed with comedy that I had to hold a preliminary round face-off between two face-offs, and the Big Name Comedies Putting It All Out There Face-Off was the unlucky loser. Pain And Gain looks interesting, but We’re The Millers appears to have been entirely built around the principle of watching a 44 year old woman take her clothes off. Instead we have Steve Carrell and Sam Rockwell versus Nick Offernan, Megan Mullally and the blink-and-you’ll-miss-her Alison Brie. The winner here is simply defined by the trailer that made me laugh the most.

WINNER: The Kings Of Summer

The Enigmatic Trailer Of Mystery Face-Off: Upstream Colour vs. Silence

I defy anyone to determine what either of these are about based purely on the trailers. No peaking at the synopses. I SAID NO PEAKING! Anyway, Upstream Colour wins this one on the entirely arbitrary basis that it’s been renamed so us simple folk in the UK are allowed to spell it correctly. (Did you know that color / colour was also once spelled culoure and coolor as well? Crazy times.)

WINNER: Upstream Colour

The Old Films Back In The Cinema Face-Off: Jurassic Park 3D vs. Plein Soleil

And finally for this month, a pair of films sneaking back into cinemas, both literary adaptations (Crighton and Highsmith respectively), but that’s about where the similarity ends. Also sneaking back into cinemas this month – if you can find them – are the likes of Michael Cimino’s Heaven’s Gate and Otto Preminger’s Bonjour Tristesse.

WINNER: Plein Soleil

The Half Dozen Special: Most Interesting Looking Trailers For July (and The Rest Of) 2013

Half way through the year, and it’s been a mixed year so far. A decent amount of five star films, but the quality layer below that has been slightly thinner than in previous years, so the second half of the year has a fair amount to make up for. But as well as the midpoint of the year, July marks another milestone: it’s the fiftieth Half Dozen that I’ve written for the blog.

Fifty collections of trailers, from the monthly specials to Superbowl reviews, annual lists of all the trailers I’ve seen at the Cambridge Film Festival and FrightFest and even a Tony Scott obituary special. From the highs of annual award winners including The Social Network, Submarine and The Imposter to the lows of fantastically cheesy trailers such as Killer Elite and Elephant White, it’s now become a monthly ritual to watch every trailer for films coming out to try to find the cream of the crop, and even if no-one reads this, then it’s helped me to uncover a few cinematic gems I wouldn’t have otherwise tried.

But if you are reading this, then you’ll be expecting some trailers, and to mark the 50th anniversary I’ve not only trawled through the whole of July, but picked out the most enticing trailers for each month for the rest of the year.

July

Blancanieves

Clearly inspired by The Artist, because no other movie has ever been made in black and white or without sound, Blancanieves translates as Snow White. Yep, it’s a Spanish Snow White with bullfighting, and if that’s not enough of a hook for you, you may wish to check your pulse to see if you’re still alive.

Pacific Rim

Long time readers of the blog will know that I like my blockbusters big, dumb and full of fun; I’m a fan of Independence Day and not ashamed to admit it. I can remember a friend telling me he didn’t get on with that particular film after the first act and the trailers had a more serious vibe and then it laid on the cheese, but in my view you can’t really do something of this scale without a bit of Stilton or Wensleydale. Early reports suggest that might not be the case, which will be a cheesy shame.

We Steal Secrets: The Story Of Wikileaks

The second documentary of the year from master documentarian Alex Gibney, this follow up to Mea Maxima Culpa will hopefully be distinguished in one key respect – hopefully I’ll actually manage to catch this one.

The World’s End

Two trailers were released for this, the upcoming closer to the informal Three Colours Cornetto trilogy. One has a casual voiceover from Simon Pegg, but this international trailer has the full-on voiceover man, and you’ve never heard someone make the words “pub crawl” sound quite so incongruous. (Although, looking for ideas of what to do for my 40th next year, maybe finding four mates to do a 12 pub crawl? Perhaps a 12 cinema crawl is more my speed.)

Frances Ha

If you, like me, have a high tolerance for kooky and mumblecore, then you’ll very much be looking forward to the latest from Noah Baumbach and Greta Gerwig. If those names strike fear into your heart, you’ll be turning this trailer off after around 10 seconds.

The Wolverine

I bear the scars of battle. I’ve seen X-Men: The Last Stand. I’ve seen X-Men Origins: Wolverine. I wasn’t looking forward to this one at all. Yet somehow this trailer has, just about, revitalised my interested, and I will be very cautiously optimistic come the end of the month. Also, just in case you weren’t convinced, here’s Hugh Jackman to really sell it to you. If the star of his own movie thinks it’ll be good, who am I to argue?

August

Plenty of potential for August with the Alan Partridge movie, Matt Damon and Jodie Foster in Neill Blomkamp’s latest Elysium, a Morgan Spurlock doc on One Direction and a David Bowie exhibition on film. But the one which has me most in anticipation is the critical Marmite that is Nicolas Winding Refn’s latest. Luke Evans dropped out to be in The Hobbit, giving us another dose of brooding Gosling. Tasty.

Only God Forgives

September